The Sovereign Counterattack: Surviving the Eskom Green Offensive

Why the launch of Eskom Green mathematically obsoletes standard intermittent private solar pipelines and the exact BTM defection mandates Deal Desks must execute to survive the sovereign counterattack.

The Market Anchor On June 9 2026 Eskom officially launched its highly anticipated renewable energy subsidiary known as Eskom Green. Armed with a mandate to scale up to 32 gigawatts of utility generation the new entity was heavily praised by the mainstream financial press. Pundits celebrated the agile transition of a legacy monopoly.

The forensic commercial reality is not a green transition. It is a targeted execution of the private Independent Power Producer market.

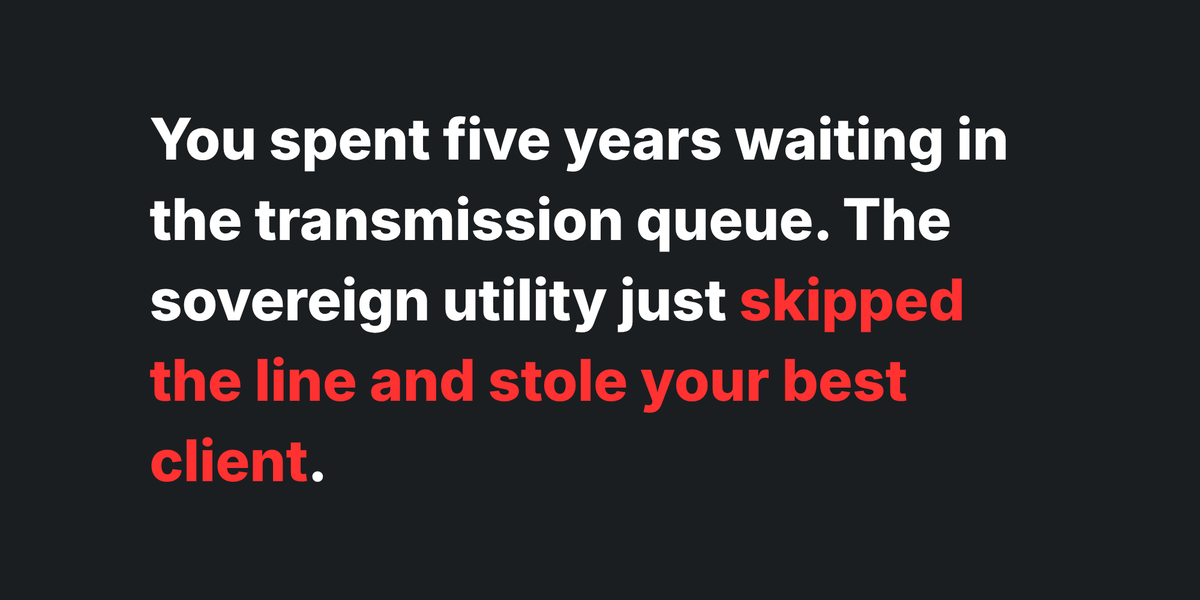

Eskom recognized that private developers were systematically stripping away their most profitable heavy industrial off takers. To stop the hemorrhage Eskom Green weaponized the exact chokepoints that paralyze private development. They are utilizing the existing high voltage switchyards at retiring Mpumalanga coal plants. While private IPPs wait half a decade for grid connection approvals Eskom Green physically bypasses the queue by plugging directly into fully permitted legacy infrastructure.

More lethally Eskom Green is not selling pure solar. They are blending their new solar and wind yields with their legacy pumped hydro and BESS fleets. They are offering Tier 1 mining and commercial clients a perfectly flat 24/7 green baseload tariff.

The Multidisciplinary Blast Radius A standard corporate Power Purchase Agreement relies on pitching a volumetric energy discount. When the sovereign state enters the market with zero interconnection delays and a vastly superior 24/7 dispatchable generation profile the standard private financial model violently collapses.

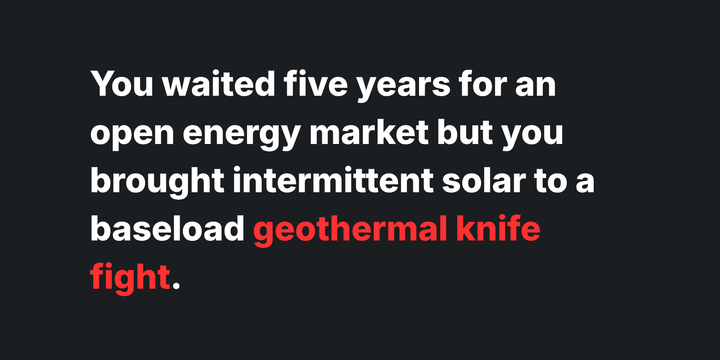

- The IPP and Developer Risk: Your entire sales strategy is mathematically obsolete. You cannot pitch an intermittent daytime only solar array to a deep level platinum mine if Eskom Green is offering them 100 percent renewable 24/7 baseload at a highly competitive blended rate. Your multi million dollar pipeline is dead on arrival.

- The Lender Risk: Infrastructure debt sized on the assumption of capturing Tier 1 corporate wheeling contracts is completely unbankable. If the private Special Purpose Vehicle cannot secure or retain heavy industrial off takers because they are continually outbid by the sovereign utility the Debt Service Coverage Ratio is immediately exposed to fatal default.

- The Aggregator Risk: Private energy traders aggregating intermittent solar assets are mathematically exposed. To provide a firm profile to their corporate clients they must buy expensive balancing power on the open market. Eskom Green utilizes depreciated legacy pumped hydro to balance their profile completely destroying the private aggregator margin.