The Insurance Void: Surviving the Defective Design Denial

Why severe flash flooding at the Tororo solar array triggered a massive defective design claim denial from insurers and the exact LEG 3 insurance clauses Deal Desks must mandate to survive the hydrology void.

The Market Anchor On April 11 2026 the Uganda Electricity Distribution Company Limited network witnessed a brutal engineering reality at the Tororo solar array. Severe localized flash flooding along a river channel induced rapid soil liquefaction beneath three major central solar tracking rows.

The public narrative blamed unpredictable climate extremes. The forensic adjusters blamed the spreadsheet.

The shifting mud caused severe structural twisting across the heavy torque tubes. This mechanical warp triggered mass cell fracturing and cascading direct current ground insulation faults repeatedly forcing the primary 1500 volt central inverters to isolate from the network.

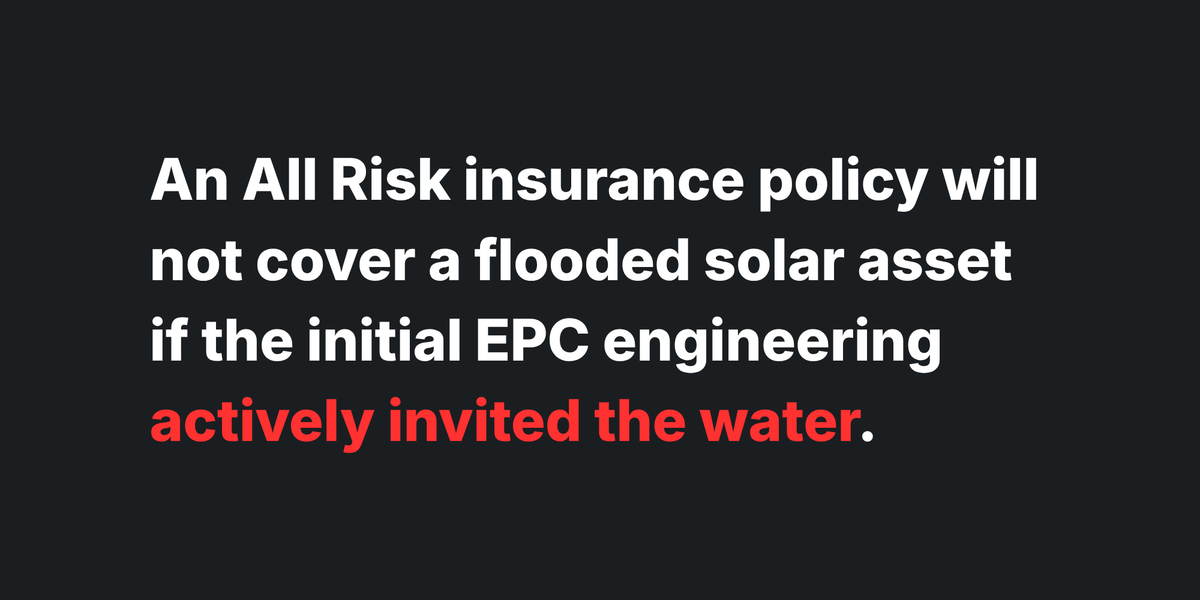

The project sponsors filed a massive remediation claim assuming their comprehensive All Risk insurance policy would cover the weather event. The insurers officially denied the claim entirely.

The underwriters cited a failure by the Engineering Procurement and Construction contractor to adhere to mandatory localized hydrological drainage and piling depth surveys. Because the EPC used generalized desktop data to save Day 1 capital expenditure they fundamentally under engineered the foundations. The developer is now holding a physically stranded asset millions of dollars in remediation costs and a voided insurance policy.

The Multidisciplinary Blast Radius When Deal Desks underwrite utility scale solar assets they assume construction risk is locked behind a lump sum contract and weather risk is locked behind an insurance policy. The Tororo event proves that if your ground engineering is flawed your legal protection is an illusion.

- The Developer and IPP Risk: The developer is trapped in a liquidity nightmare. The asset cannot generate revenue to meet the Power Purchase Agreement volumetric targets but the debt amortization schedule remains rigid. Without an insurance payout the Special Purpose Vehicle faces an immediate debt default.

- The EPC Risk: The contractor will attempt to declare the flash flood an unforeseeable act of God and invoke a Force Majeure clause to escape liability. If the Employer Requirements were too broad the developer has exactly zero legal leverage to force the contractor to rebuild the foundations at their own expense.

- The Lender Risk: The Credit Committee approved the debt facility based strictly on the presence of an All Risk policy. The moment the insurer invokes a defective design exclusion the entire risk profile of the debt facility violently shifts from secured infrastructure to unsecured liability.